The 2025–26 financial year is shaping up to be one of stability rather than change in personal tax rates.

However, SMEs should not get complacent: there are still important considerations around instant asset write-offs, ATO compliance priorities, and superannuation changes. This article explains the current rules, what has(and hasn’t) changed, and how businesses can prepare.

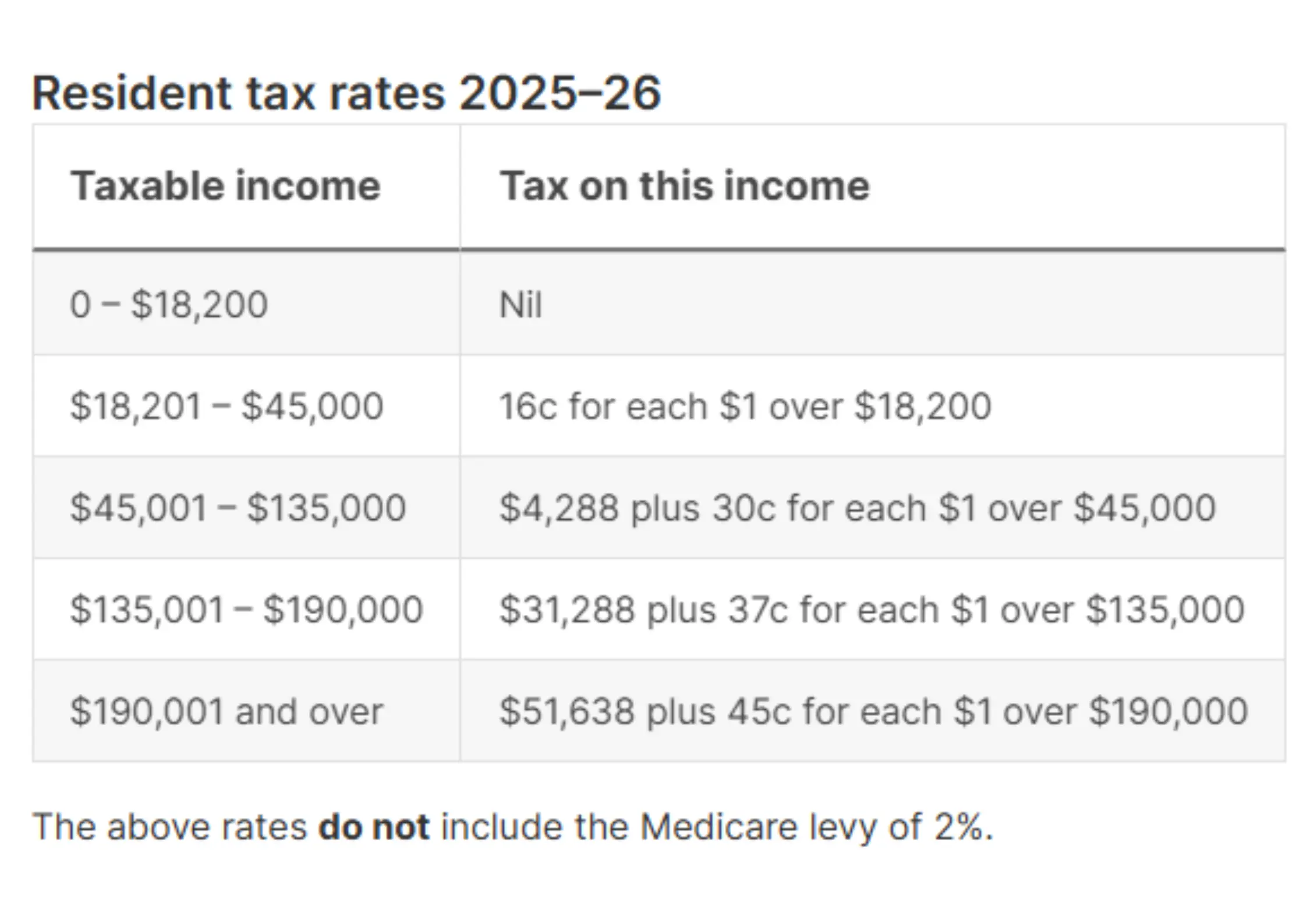

The Individual Tax brackets from 1 July 2025 remain unchanged from the prior Financial Year as follows;

SME implications:

· Businessowners operating via companies and trusts should not expect bracket relief.

· Tax planning will continue to rely heavily on distribution strategies, company tax rates, and super contributions.

· Any new reform proposals are more likely to surface in the 2026 Federal Budget, so SMEs should remain agile.

The instant asset write-off has been a moving target in recent years, with thresholds and eligibility shifting almost annually.

SME implications:

Division 7Aloans remain a critical area for compliance. The benchmark interest rate, used to calculate minimum repayments on shareholder loans, has been volatile:

This is a significant jump compared to historic levels (as low as 4.52% in 2021).

SME implications:

Consideration: Review shareholder loan arrangements now. Consider repaying or refinancing to reduce exposure to higher Division 7A interest rates.

The ATO has flagged enhanced compliance activity in 2025–26, particularly around:

Consideration: SMEs using trusts, intercompany or inter-entity loans, or property ventures should seek early advice to ensure documentation and compliance are watertight.

Consideration: Plan contribution strategies before year-end to optimise deductible contributions and retirement savings.

To prepare and finish strong for 2025–26:

The new financial year isn’t just about new tax rates – it’s about ensuring your SME is positioned to make the most of opportunities and avoid compliance pitfalls. With proactive planning around remuneration, asset purchases, and business structures, SMEs can enter 2025–26 with confidence.

At Aspira, we’re hereto help you map the impact, plan ahead, and stay compliant. If you’d like tailored advice for your business, now is the time to start the conversation.

.svg)

116/10-16 Kenrick St, The Junction NSW 2291

32 St Andrews St, Maitland NSW 2320

(02) 4924 0000